ESTABLISHMENT PHASE

Life Planning

- Career exploration

- Marriage

- Children

- Establishment of budget

- Due to increased debt

- Savings for a house

- First house

- Establish emergency fund

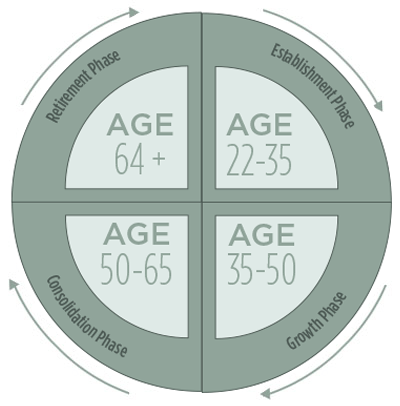

Lifecycle

Establishment Phase

(Age 22-35)

Premature Death Planning

- Debt liquidation fund

- Mortgage insurance

- Spouse income requirements

- Children’s Insurance

- Will planning

GROWTH PHASE

Life Planning

- Bigger house

- Larger Family

- Increased debt

- Concentration on Career

- Growth or redirection

- Children’s education fund

- Emphasis on accumulation

of capital

Lifecycle

Growth Phase

(Age 35-50)

Premature Death Planning

- Premature Death Planning

- Debt liquidation fund

- Increased mortgage

insurance - Increased spousal income

needs - Child/home care fund

- Immediate money fund

(Estate settlement) - Will Planning

CONSOLIDATION PHASE

Life Planning

- Financing children’s education

- Assessing current investments

with a view towards retirement - Children leave home

- Possible purchase of smaller

house - Debt reduction

- Income splitting between

spouses - Shift in emphasis from job to

quality of life

Lifecycle

Growth Phase

(Age 50-65)

Premature Death Planning

- Financing children’s education

- Assessing current investments

with a view towards retirement - Children leave home

- Possible purchase of smaller

house - Debt reduction

- Income splitting between

spouses - Shift in emphasis from job to

quality of life

RETIREMENT PHASE

Life Planning

- Financing children’s education

- Assessing current investments

with a view towards retirement - Children leave home

- Possible purchase of smaller

house - Debt reduction

- Income splitting between

spouses - Shift in emphasis from job to

quality of life

Lifecycle

Growth Phase

(Age 65 – ?)

Premature Death Planning

- Financing children’s education

- Assessing current investments

with a view towards retirement - Children leave home

- Possible purchase of smaller

house - Debt reduction

- Income splitting between

spouses - Shift in emphasis from job to

quality of life